Home Loan Documents Checklist

Applying for a home loan can feel complicated, especially when banks ask for multiple documents during the approval process.

Many home loan applications get delayed simply because:

- documents are incomplete,

- paperwork is incorrect,

- or applicants do not understand what banks actually require.

Proper documentation plays a major role in:

- faster approvals,

- smoother verification,

- better loan eligibility,

- and reduced processing delays.

This complete guide explains:

- all documents required for home loan,

- documents for salaried and self-employed applicants,

- property-related paperwork,

- common mistakes to avoid,

- and tips for smooth approval.

Why Documents Are Important for Home Loan Approval

Banks provide large amounts of money through home loans.

Before approving a loan, banks carefully verify:

- identity,

- income,

- repayment capacity,

- employment stability,

- property ownership,

- and financial history.

Documents help banks evaluate:

Whether the applicant can repay the loan safely.

Proper documentation increases trust and reduces risk for lenders.

Main Categories of Home Loan Documents

Home loan documents are generally divided into:

- identity documents,

- address proof,

- income proof,

- bank statements,

- employment documents,

- property documents,

- and financial records.

Requirements may vary depending on:

- bank,

- applicant profile,

- property type,

- and loan amount.

Basic Documents Required for All Applicants

These documents are commonly required for both salaried and self-employed applicants.

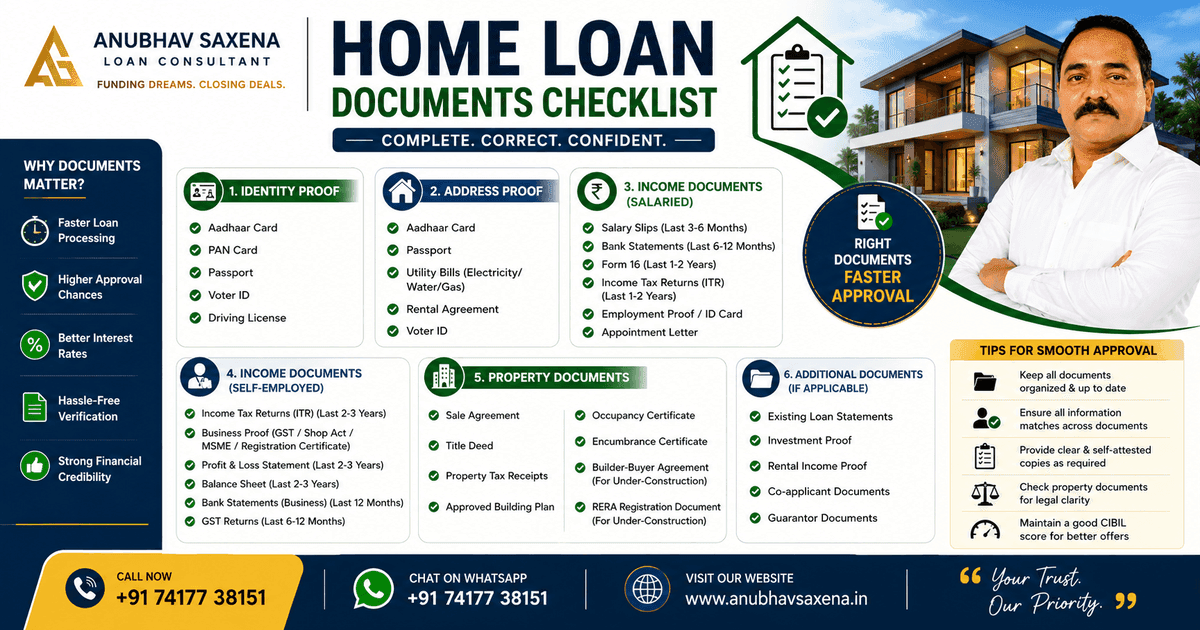

1. Identity Proof

Banks require valid government-issued identity proof.

Accepted documents usually include:

- Aadhaar Card

- PAN Card

- Passport

- Voter ID

- Driving License

Why PAN Card Is Important

PAN card is mandatory for most loan applications because banks use it to:

- verify financial records,

- check credit history,

- and access CIBIL score.

2. Address Proof

Applicants must provide current address proof.

Accepted documents may include:

- Aadhaar Card

- Passport

- Utility Bills

- Driving License

- Rental Agreement

- Voter ID

Address proof should ideally match:

- application details,

- and bank records.

3. Passport Size Photographs

Banks usually require:

2–8 recent passport-size photographs

depending on the lender’s process.

4. PAN Card

PAN card is compulsory for:

- income verification,

- tax records,

- and financial tracking.

Without PAN:

- loan processing becomes difficult,

- and approval delays may occur.

Income Documents for Salaried Employees

Salaried applicants usually need fewer documents compared to self-employed individuals.

1. Salary Slips

Most banks ask for:

Last 3–6 months salary slips

Salary slips help banks analyze:

- monthly income,

- deductions,

- and employment consistency.

2. Bank Statements

Banks generally require:

Last 6–12 months bank statements

Bank statements help verify:

- salary credits,

- existing EMIs,

- financial behavior,

- and repayment capacity.

3. Form 16

Form 16 confirms:

- salary structure,

- income tax deductions,

- and employment details.

It strengthens income verification.

4. Income Tax Returns (ITR)

Some banks ask for:

Last 1–2 years ITR

especially for:

- higher loan amounts,

- additional income,

- or special financial profiles.

5. Employment Proof

Employment verification may include:

- employee ID card,

- appointment letter,

- HR confirmation,

- or office email verification.

Banks prefer:

- stable employment,

- reputed companies,

- and regular income flow.

Documents Required for Self-Employed Applicants

Self-employed applicants undergo stricter financial scrutiny.

Banks analyze:

- business stability,

- income consistency,

- and repayment capacity carefully.

1. Income Tax Returns

Most banks require:

Last 2–3 years ITR

for self-employed borrowers.

This helps assess:

- annual income,

- business growth,

- and tax compliance.

2. Business Proof

Accepted business documents may include:

- GST registration,

- Shop Act License,

- MSME registration,

- Partnership Deed,

- Company Incorporation Certificate,

- Trade License,

- or Professional Practice Certificate.

3. Profit & Loss Statement

Banks often ask for:

- audited financial statements,

- balance sheets,

- and profit-loss accounts.

These documents show:

- business profitability,

- turnover,

- and financial health.

4. Business Bank Statements

Usually:

Last 12 months bank statements

are required.

Banks analyze:

- cash flow,

- business stability,

- and transaction consistency.

5. GST Returns

GST returns help banks understand:

- business turnover,

- operational scale,

- and financial credibility.

Property Documents Required for Home Loan

Property verification is one of the most important stages of home loan approval.

Banks carefully verify:

- ownership,

- legal status,

- and market value.

1. Sale Agreement

This document contains:

- buyer details,

- seller details,

- property value,

- and transaction terms.

2. Title Deed

Title deed confirms:

Legal ownership of property

Banks carefully examine ownership history.

3. Property Tax Receipts

These verify:

- tax compliance,

- and municipal records.

4. Approved Building Plan

Banks require municipal approval documents for:

- apartments,

- independent houses,

- and construction projects.

5. Occupancy Certificate

This confirms:

The property is legally ready for occupation

Important for ready-to-move properties.

6. Encumbrance Certificate

This verifies:

- property is free from legal liabilities,

- disputes,

- or existing loans.

7. Builder Documents (For Under-Construction Property)

Banks may ask for:

- builder-buyer agreement,

- RERA registration,

- project approvals,

- and construction permissions.

Additional Documents Sometimes Required

Depending on the profile, banks may ask for:

- existing loan statements,

- investment proof,

- rental income proof,

- co-applicant documents,

- guarantor documents,

- or agricultural income proof.

Documents Required for Joint Home Loan

When applying jointly:

- both applicants must submit documents,

- including identity,

- income proof,

- and bank statements.

Joint applications may improve:

- loan eligibility,

- and approval chances.

Importance of CIBIL Score Documents

Banks check:

Credit score and repayment history

before approval.

Strong CIBIL score improves:

- eligibility,

- interest rate,

- and approval speed.

Common Reasons Home Loan Gets Delayed

Incomplete Documentation

Missing paperwork is one of the biggest reasons for delays.

Incorrect Information

Mismatched:

- signatures,

- addresses,

- or financial details

can create verification issues.

Weak Financial Proof

Insufficient income proof may reduce approval chances.

Property Legal Issues

Unclear ownership or missing approvals can delay processing significantly.

Poor Credit History

Low CIBIL score increases scrutiny.

Tips for Smooth Home Loan Documentation

Organize Documents Early

Prepare paperwork before applying.

This speeds up approval significantly.

Keep Photocopies Ready

Banks may require:

- self-attested copies,

- and multiple document sets.

Ensure Accurate Information

All details should match across:

- PAN,

- Aadhaar,

- bank statements,

- and application forms.

Maintain Good Financial Records

Clean financial history improves trust.

Check Property Legality

Always verify:

- approvals,

- ownership,

- and legal clearance.

Digital Documents vs Physical Documents

Many banks now support:

- digital uploads,

- online KYC,

- and e-verification.

However:

- physical verification may still be required during final processing.

Home Loan Documents for NRIs

NRIs may additionally require:

- passport,

- visa documents,

- overseas income proof,

- employment contract,

- and international bank statements.

Home Loan Processing Timeline

Typical approval timeline:

| Stage | Approx Time |

|---|---|

| Initial Verification | 2–5 days |

| Income Assessment | 3–7 days |

| Property Verification | 5–10 days |

| Final Approval | 7–15 days |

Proper documentation can speed up processing significantly.

Frequently Asked Questions

Is PAN card mandatory for home loan?

Yes.

PAN card is generally compulsory for home loan processing.

How many months bank statement is required?

Most banks require:

6–12 months bank statements

Is salary slip mandatory for salaried applicants?

Yes.

Salary slips help banks verify stable income.

Can self-employed applicants get home loan?

Absolutely.

However, documentation requirements are usually stricter.

What documents are needed for under-construction property?

Commonly required:

- builder agreement,

- project approvals,

- RERA documents,

- and construction permissions.

Final Thoughts

Home loan documentation may seem complicated initially, but proper preparation makes the process much smoother.

Banks mainly want to verify:

- identity,

- repayment ability,

- financial stability,

- and property legality.

Well-organized documents help:

- reduce delays,

- improve approval chances,

- and speed up loan processing.

Whether you are:

- salaried,

- self-employed,

- business owner,

- or first-time home buyer,

understanding documentation requirements can save:

- time,

- stress,

- and unnecessary rejection risk.

Need Home Loan Assistance?

Anubhav Saxena provides expert support for:

- Home Loans

- Business Loans

- Project Finance

- Agriculture Loans

- CC Limit & OD Limit

Get professional help for:

- documentation,

- eligibility guidance,

- bank coordination,

- and faster approvals.

Funding Dreams. Closing Deals.